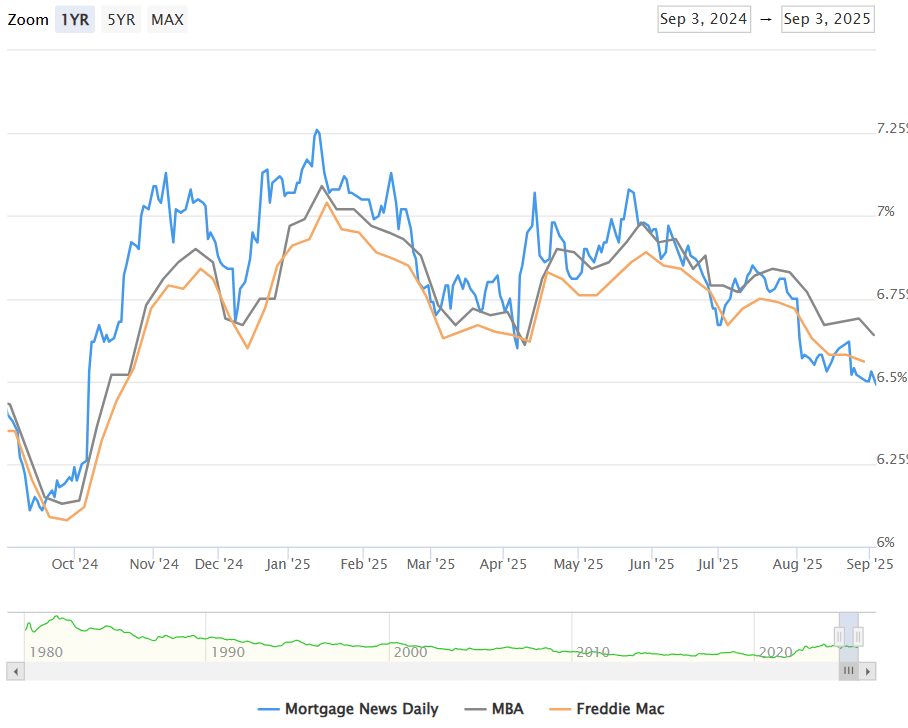

Mortgage Rates Hit an 11-Month Low

buyers Connexa Real Estate September 4, 2025

buyers Connexa Real Estate September 4, 2025

If you’ve been waiting and watching mortgage rates for a sign, here’s some good news: rates have dipped to their lowest point in nearly a year. The average 30-year fixed mortgage rate now sits around 6.45%–6.49%, down from the 7%+ highs we saw earlier this year.

But before you get too excited, let’s break down the current mortgage rate trends—and what they mean if you’re thinking about buying, selling, or refinancing.

The short answer: the job market.

Recent reports show that there are now more unemployed workers than job openings, a reversal from the past several years. Since the Federal Reserve watches labor data closely, softer job numbers ease inflation concerns. This brings down bond yields, which helps pull mortgage interest rates lower.

That said, economists warn against expecting major drops anytime soon. Rates have eased slightly, but changes are measured in fractions of a percent—not whole points.

Here’s where average mortgage rates stand as of early September 2025:

30-Year Fixed Mortgage Rate: 6.45% (last week: 6.44%)

15-Year Fixed Mortgage Rate: 5.40% (last week: 5.43%)

30-Year Jumbo Mortgage Rate: 6.65% (unchanged from last week)

For perspective:

In January 2025, the 30-year fixed rate peaked above 7.25%.

Today, rates are in the mid-6% range, which is the lowest level in nearly 11 months.

If you’re holding a rate from the last few years (3–4%), refinancing doesn’t make sense yet. But if you purchased at the peak of 7%+, this dip may create room for savings—especially if rates fall further.

Here’s the honest truth: while mortgage rates are lower, the day-to-day changes are small. Your monthly payment may not feel dramatically different compared to last week.

That said, even small improvements matter. On a $300,000 loan:

At 6.45% → about $1,887/month

At 7.25% (earlier this year) → about $2,046/month

That’s a difference of about $159 each month—not massive, but enough to impact affordability and loan approval.

More affordable payments bring more buyers back into the market. Even small drops in mortgage rates can increase demand, which may lead to stronger offers and faster sales for sellers ready to list.

This week is “Jobs Week,” with several key reports due, including the major monthly jobs report on Friday.

And here’s the key takeaway: bigger moves in mortgage rates could follow—but they can go either direction. A weaker labor market could push rates lower, while stronger-than-expected data could send them higher again.

Mortgage rates are sitting at their lowest point in nearly a year, hovering in the mid-6% range. That’s good news for buyers and sellers alike—but don’t expect massive overnight changes.

The smartest move? Stay informed, crunch the numbers, and act when the timing makes sense for your situation—not just the headlines.

Places to Celebrate Dad (Where He Won’t Wander Off)

local

Your ROI Investment Guide

Ready to buy, sell, or invest in Virginia real estate? Reach out to our experts today to start a conversation. We're here to help.